The Secrets Behind Credit Card Profitability: Exploring How They Make Money?

Are you ready to unveil the mystery behind those shiny pieces of plastic in your wallet? Brace yourself for a deep dive into the captivating world of credit card profitability. From enticing reward programs to hidden fees, this blog post uncovers the secret mechanisms that unlock immense profits for credit card companies.

Get set to unravel how these financial superheroes make money and discover strategies you can leverage as we embark on an eye-opening exploration into the mysterious realm of credit cards!

Table of Contents

What is a Credit Card Transaction?

Credit cards are one of the most popular payment methods in the world. According to the 2016 CreditCards.com Annual Report, Americans held $2.1 trillion in credit card debt as of December 31st, 2016. In order for a credit card issuer to make money from a credit card transaction, they must abide by certain procedures and policies.

A credit card transaction is made when a customer uses their credit card to purchase something from a merchant. The issuer of the credit card charges the merchant for what was purchased and pays the customer back through their regular billing cycle. Issuers typically earn interest on transactions, which helps cover expenses associated with issuing and administering cards such as monthly fees and increased marketing costs.

In order for an issuer to make maximum profit from a credit card transaction, they must adhere to a number of important rules:

- The issuer must assess risk when approving a customer for a credit card account: high-risk customers are less likely to be approved for a credit card account due to their history of missed payments or bankruptcy filings. Therefore, issuers want to approve cards only for customers who have a good chance of paying back their debts in full each month.

- The issuer must charge merchants more for transactions carried out with high-risk customers: these customers are more likely to default on their loans and owe more money than average when they do pull out their cards. Merchants who accept payment cards via magnetic stripe (where data is transferred directly between the reader on the card and the merchant’s computer) are typically charged more for these transactions.

- The issuer must monitor customer transactions: to ensure that customers are using their cards as intended and not simply spending money they don’t have, issuers track all card activity, including purchases, cash withdrawals, and balance inquiries. This data is then used to determine whether or not customers are in a good financial position to repay their debt.

- If the issuer believes that a customer is at risk of defaulting on their debt, they may prohibit them from making any more purchases using their credit card.

- If a customer defaults on their credit card debt, the issuer may suspend or cancel his or her card privileges.

Intro to Fee Structures

There are a variety of fee structures in place for credit cards, and understanding how they work can help you optimize your card usage. In this article, we’ll explore the three most common fee structures and their effects on card profitability.

The Most Common Fee Structure

- Minimum Spend Requirement: This is the simplest fee structure, where cards require users to spend a set amount of money within a set period before earning rewards. This can be advantageous for users who are budget-minded or who want to minimize risk in their spending due to the associated minimum spend requirement.

- Ongoing Fees: In contrast to the minimum spend requirement, ongoing fees permit users unlimited spending without penalty, but they must pay periodic charges to maintain their rewards status. Cards with ongoing fees tend to earn higher reward rates as customers borrow more against them over time.

- Redemptions: Some cards offer redemption features that allow customers to convert points into miles and cash back, which can help offset the associated fees.

The Most Popular Fee Structure

- Introductory Rate: This is the most common fee structure in use today, where cards offer introductory rewards rates for a set period after which the rate increases. This can be advantageous for users who want to maximize their gains from card usage without bearing unnecessary risk.

- Ongoing Fees and Rewards: Another option is to include ongoing fees and rewards, where cards require customers to pay periodic charges as well as endure regular rewards offers, even after their introductory period has ended. Cards with this structure generally offer higher reward rates than those that only have an intro rate.

- Annual Fees: Some cards also include annual fees, which charge customers a fixed amount every year in addition to any associated reward rates. While this option can be more expensive than those with introductory or ongoing fees, it can also offer more stability and security for customers who want to maintain their benefits from card usage over an extended period.

The Most Efficient Fee Structure

- All fees: This is the most efficient fee structure, where all fees associated with card usage are included in the rewards rate. This may be advantageous for users who want to maximize their earnings from card usage without paying unnecessary fees.

- Ongoing Fees and Rewards: Another option is to include ongoing fees and rewards, where cards require customers to pay periodic charges as well as endure regular rewards offers, even after their introductory period has ended. Cards with this structure generally offer higher reward rates than those that only have an intro rate.

- Annual Fees: Some cards also include annual fees, which charge customers a fixed amount every year in addition to any associated reward rates. While this option can be more expensive than those with introductory or ongoing fees, it can also offer more stability and security for customers who want to maintain their benefits from card usage over an extended period.

How do Credit Cards Process Payments?

Credit cards are one of the most popular payment methods in the world. In fact, according to The Nilson Report, credit card processing was worth $128.7 billion in 2017. This means that credit cards are responsible for a significant amount of money being moved around the world each year.

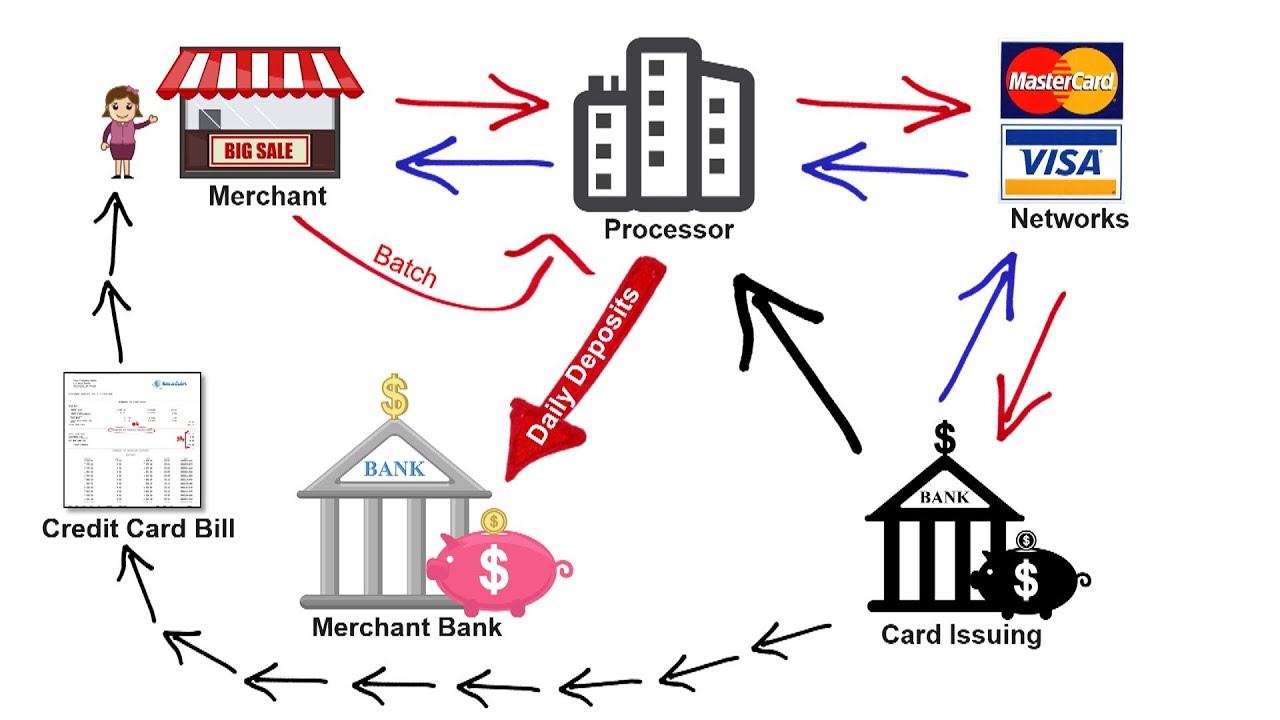

To understand how credit cards work, it’s important to understand how payments are processed. Payments are considered complete when they’re transferred from one account to another. This process typically happens through a network of banks and financial institutions.

Each bank performs different steps to complete payment. For example, some banks might take responsibility for confirming the transaction, while other banks might process the payment and send the funds to the recipient’s bank account.

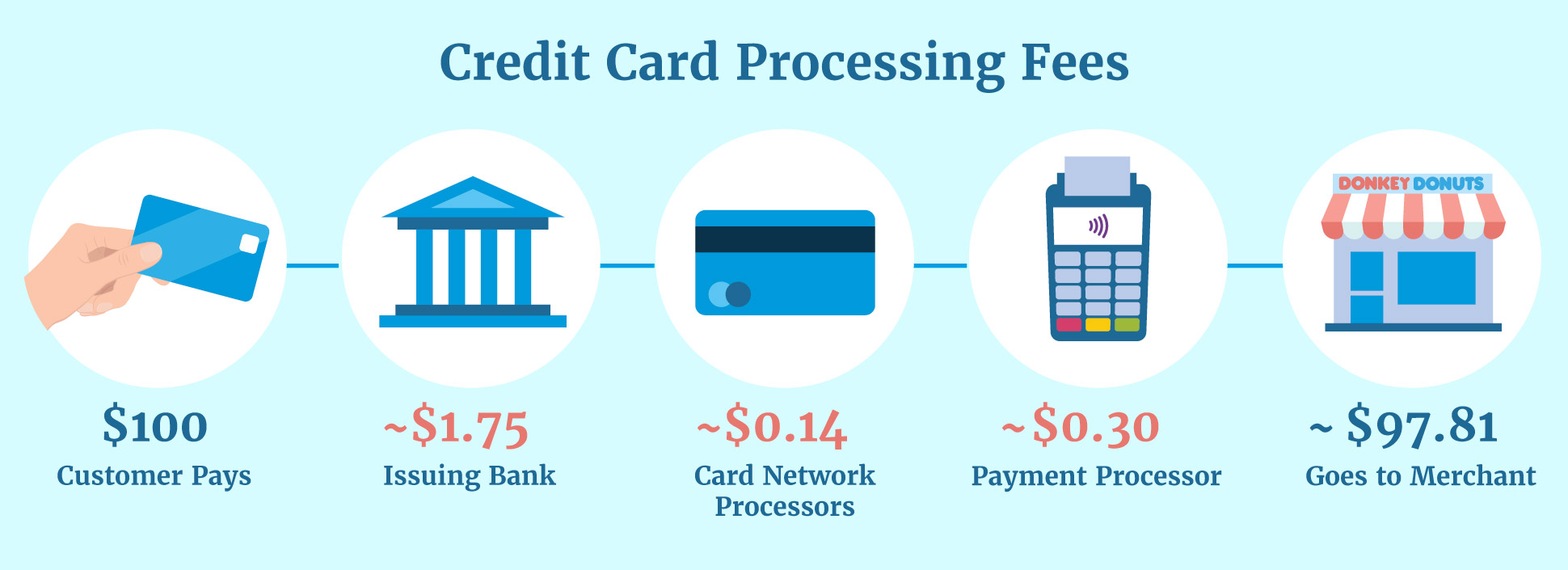

Credit card companies rely on three main mechanisms to make money: interchange fees, seller fees, and loan interest rates. Each mechanism has an impact on how profitable a card company is overall.

How Credit Card Companies Make Money?

Credit card companies make money in a variety of ways. Here are the top four:

- Fees and interest: Credit card companies charge fees for using their services, including interest on balances that go unpaid. In addition, many cards also assess late fees or add surcharges for missed payments.

- Marketing and advertising: Credit card issuers spend millions of dollars each year marketing and advertising their products to consumers, particularly by sponsoring major sporting events and promoting special offers.

- Processing charges: Some credit cards charge processing fees for each purchase, which can add up if you make a lot of purchases with your card.

- Making loans: Credit card companies also make loans to customers who need a short-term financial boost, such as when they are facing an unexpected expense or need to cover some immediate travel expenses.

Many people think of credit cards simply as tools for borrowing money – but credit cards can also be profitable businesses in their own right. Here’s how credit card companies make money:

Fees and interest: Credit card companies charge fees for using their services, including interest on balances that go unpaid.

In addition, many cards also assess late fees or add surcharges for missed payments. They also generate additional income through the sale of these fees to third parties such as banks that provide merchant accounts services to retailers.

Marketing and advertising: Credit card issuers spend millions of dollars each year marketing and advertising

Conclusion

Credit card companies make money by charging interest on credit cards and fees from other activities like renewals, application processing, and foreign transactions. This article will explore how these activities work and the mechanisms that credit card companies use to generate profits. Understanding how these companies operate can help you protect yourself from exploitation and save you money in the long run.